The Macro Technology Paradigm

I. The Precedent of Ubiquity: “Everything is Technology”

Traditional asset allocation playbooks are fundamentally broken because they treat “Technology” as a standalone, isolated vertical slice of the broader market. In reality, technology is the universal solvent that targets, invades, and completely re-architects legacy industries.

To understand where global capital is moving, we must analyze how technology behaves historically. As Packy McCormick outlines in his landmark thesis, Everything is Technology, a sector is only labeled “technology” while its core operating model is a novel, un-ubiquitous differentiator. Once that technology achieves global scale, deep integration, and total adoption, the market ceases to look at it as an exotic innovation—it simply receives its own vertical industry name.

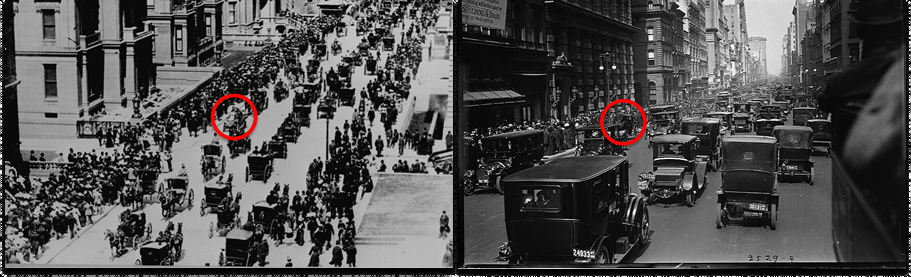

The ultimate visualization of this shift is captured in the classic comparison of the New York City Easter Parade on Fifth Avenue:

Fifth Avenue Easter Parade in NYC, 1900 (left) vs 1913 (right)

When Henry Ford introduced the Model T, he wasn’t launching a traditional manufacturing company; he was running the frontier, hyper-growth deep tech startup of the early 20th century. McCormick captures the reality of this transition perfectly:

“Ford introduced the Model T in 1908. If he’d asked customers what they wanted, he quipped, they would have asked for faster horses. Just five years later, the de-equinization of New York City was practically complete. The Model T was both faster and cheaper than horses, and it didn’t shit all over the street.”

By 1919, the legacy “Carriages & Wagons” market was rendered entirely obsolete, sitting at a meager $118.2 million total valuation according to historical data from the US Census Bureau Manufacturing Bulletin.

Crucially, technology didn’t just steal horse carriage market share — it fundamentally expanded the underlying economic pie. In that same period, Ford manufactured over 900,000 Model Ts priced at roughly $360 each, generating $324 million in revenue from a single vehicle model, as verified by the historical Harvard Business Review Ford Vital Statistics Dataset. A single tech-driven entrant generated more than double the aggregate product value of the entire industry it had just displaced. By the time this technology became completely ubiquitous, it earned its own distinct vertical name: the “Automotive Industry.” Reflecting the staggering scale of this structural historical shift, by the end of 2003, the world’s twelve largest automakers sported a combined market cap of ~$450 billion, a metric highlighted in Packy McCormick’s ‘Everything is Technology’ Analysis.

II. Disruption, Rinse, Repeat: Why Technology Never Stops Winning

This historical expansion reveals a deeper structural phenomenon regarding how value is categorized by Wall Street. Because the 20th-century automotive giants eventually evolved into slow-moving, traditional manufacturing businesses, that valuation was no longer considered “tech market cap.” It fell completely outside of Venture Capital Addressable Value (VCAV) — the total economic enterprise value that venture capital can systematically target, disrupt, and capture.

Exactly one century after Henry Ford’s initial disruption, the automotive industry had become sclerotic, defined by legacy dealership networks and rigid hardware supply chains. In other words, they were primed for another disruption. That disruption was Elon Musk and Tesla. If Elon Musk had asked customers what they wanted in 2003, they likely would have requested “faster, more fuel-efficient internal combustion engine (ICE) SUVs.”

Like Henry Ford, Musk did not ask. He introduced a software-defined electric vehicle platform.

By July 2020, this alternative approach reached a historical tipping point when Tesla officially bypassed Toyota to become the most valuable automaker in the world. Tesla did not just disrupt ICE manufacturing; it pulled the entire automotive sector straight back into the technology paradigm, and right back into VCAV.

III. The Tech Inversion: The Modern Cross-Sector Reality

This twin-disruption automotive case study is not an anomaly; it is a repeatable economic law. Every industry currently dominated by large, legacy incumbents will inevitably come to be dominated by technology platforms.

When we audit the dominant market cap leaders across every major economic vertical as of May 2026, we find that the true category kings are all technology platforms leveraging high-margin software, internet distribution, and advanced computing architectures to maintain their moats:

Global Sector Audit

|

Traditional Vertical Category

|

Sector Leader

|

Market Value (May 2026)

|

The "Tech in Disguise" Reality

|

|---|---|---|---|

|

Information Technology

|

Nvidia

|

$5.41T

|

Pure-play computational infrastructure, algorithmic web distribution engines, and foundation compute layers driving global AI deployment.

|

|

|

Apple

|

$4.38T

|

|

|

|

Alphabet

|

$4.81T

|

|

|

Communication Services

|

Meta

|

$1.56T

|

Nominally classified as a "media and advertising agency," but operationally an AI-driven distribution network.

|

|

Consumer Discretionary

|

Amazon

|

$2.85T

|

Amazon operates as a global utility network via AWS cloud infrastructure.

|

|

|

Tesla

|

$1.49T

|

A real-world AI platform whose tech multiple is anchored by its FSD software stack (converting vehicles into high-margin computing nodes) and its Optimus humanoid robotics platform. By running a unified vision-and-control neural network architecture across both autonomous fleets and bipedal hardware, Tesla is transforming from an automaker into a generalized automation and scalable labor utility.

|

|

Health Care

|

Eli Lilly

|

$897B

|

Scaling toward a trillion-dollar valuation by programming biology through generative AI molecule-mapping and computational chemistry.

|

|

Industrials

|

SpaceX

|

$1.50T (EstimatedPrivate Market Value)

|

Dictates the entire modern aerospace, defense, and orbital communications framework via a deeply integrated software-and-hardware tech stack.

|

|

Consumer Staples

|

Walmart

|

$1.05T

|

Crossed the historic trillion-dollar threshold by converting brick-and-mortar retail into an automated, machine-learning supply chain.

|

|

Finance

|

JPMorgan Chase

|

$832B

|

Operates fundamentally as an enterprise software firm with a banking license, deploying an annual $15B+ technology budget to protect its moat.

|

IV. The Geometry of Expansion: Demolishing Static TAM

When technology enters a legacy sector, traditional public-market analysts consistently make a fatal error: they assume the Total Addressable Market (TAM) is a fixed pie.

The ultimate playbook on this miscalculation belongs to Benchmark Partner Bill Gurley. In his legendary essay, How to Miss by a Mile: An Alternative Look at Uber’s Potential Market Size, Gurley systematically dismantled Wall Street valuation models that capped Uber’s upside by measuring it strictly against the historical, localized taxi market ($5.9 billion).

As McCormick highlights, technology expands the economic pie through two distinct structural frameworks:

- Direct Displacement (eating someone else’s lunch): Competing directly in large existing addressable markets with a better, cheaper, faster product.

- Market Creation and Aggregation (cooking up its own): Creating new addressable markets out of previously fragmented ones with a better, cheaper, faster technology product in place of an analog one.

Traditional financial tools completely fail to model this dynamic. When legacy valuation models capped Uber’s value based on a static view of transport, they missed the reality that venture-backed tech can create entirely new economic addressability out of thin air. Whereas venture capitalists historically could not invest in traditional, localized car-for-hire services, they were able to back a global software rail. Tech re-architected the system and unlocked massive capital value where none previously existed.

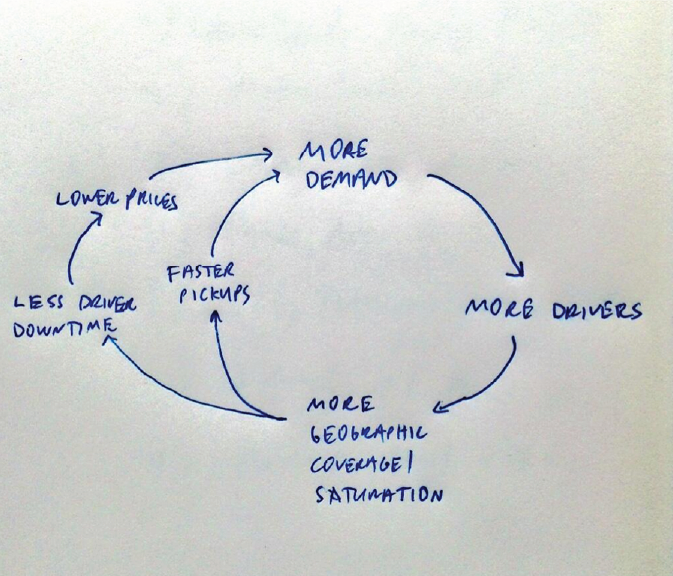

By applying David Sacks’ classic napkin flywheel sketch, Uber completely broke the constraints of the traditional transport ecosystem:

Former White House AI and Crypto Czar David Sacks’ Famous Uber Napkin Sketch

By removing the friction of physical street-hailing, introducing frictionless smartphone payments, guaranteeing real-time safety tracking, and optimizing vehicle utilization, Uber didn’t just steal legacy taxi users. It altered human behavior, turning ride-hailing into a systemic alternative to personal car ownership. Technology manufactured a market multiple orders of magnitude larger than the sector it originally targeted. Today, Uber commands an institutional market value of over $150 billion. Traditional Wall Street financial models missed the ultimate outcome by exactly 25x.

V. The Value Capture Shift: The Private Compounding Mandate

Because technology companies grow faster, scale at higher margins, and expand the underlying TAM, they generate historic amounts of wealth. However, the structural mechanism for capturing this value has permanently shifted away from public markets.

To visualize this change, we contrast the two distinct corporate eras of Elon Musk:

- The Old Playbook (Tesla): When Tesla IPO’d in 2010, it hit the public markets at a minor valuation of ~$1.5 billion. Public market retail and institutional investors were able to ride the entire explosive wave as the company scaled from an early venture phase into a trillion-dollar category king.

- The New Playbook (SpaceX): Musk’s second empire shows how the private venture ecosystem has completely matured. SpaceX has scaled entirely behind closed doors. Fueled by deep private primary rounds and robust, highly liquid institutional secondary markets, SpaceX has compounded to reach an estimated$1.50 trillion private market valuation as of May 2026.

As the company reportedly aims for an upcoming public market debut, targeting a rumored $1.75 trillion to $2.00 trillion valuation framework, the structural message to institutional LPs is undeniable: The massive 100x compounding curve is now happening before the IPO.

If an institutional portfolio relies strictly on public equities, it is structurally locked out of the primary wealth-generation phase of this generation’s foundational monopolies. Accessing top-tier venture capital early via private markets is no longer an optional alternative strategy — it is a mandatory requirement to capture elite companies during their true compounding years.

VI. The Ultimate Frontier: Why We Focus on Crypto

If everything is technology, and technology systematically targets and scales the largest asset classes on earth, then Crypto, Web3, and Blockchain represent the ultimate technical architecture for the global financial settlement layer.

Crypto venture capital has historically generated some of the most asymmetric returns across the entire venture landscape because it targets the ultimate legacy incumbent: the multi-trillion dollar financial industry.

When you supercharge this infrastructure with the current explosion of the AI x Crypto Convergence — combining decentralized high-performance compute networks with autonomous, tokenized agentic commerce — the potential TAM expands exponentially past human operational constraints.

This macro-technological conviction is precisely why Brooker has launched Brook Limited Partners Fund of Funds I. We are not simply chasing a volatile asset class; we are backing the structural professionalization of an ecosystem crossing its own historic threshold of utility.